Image

Your debt-to-income ratio (DTI) shows how much of your monthly income goes toward paying debts. A lower DTI generally means stronger borrowing power, while a higher DTI may signal that your debt load is too heavy.

Knowing how to calculate your DTI — and what qualifies as a good debt-to-income ratio — helps you prepare for big financial decisions like buying a car, applying for a loan, or refinancing.

Key takeaways

- DTI = (Monthly Debt ÷ Gross Monthly Income) × 100

- Aim for a DTI under 36% for the best borrowing opportunities.

- Improving your DTI takes time, but every small change helps.

Your debt-to-income ratio (DTI) compares how much you owe each month to how much you earn before taxes. It’s one of the ways lenders assess your ability to manage monthly payments and repay borrowed money.

Example:

If you earn $5,000 a month and pay $1,500 toward loans, credit cards, or other debts, your DTI is 30%. That means 30% of your income goes toward debt obligations.

Think of your DTI as a snapshot of how balanced your borrowing and income are. The lower the number, the more room you have in your budget for new goals or unexpected costs.

Lenders use your DTI ratio to gauge repayment ability. It helps them decide whether to approve you for credit cards, personal loans, auto loans, or mortgages — and on what terms.

Each lender has its own cutoff points. For example, mortgage lenders often prefer a DTI under 43%, while credit card or personal loan providers may allow slightly higher ratios for strong applicants.

By knowing your DTI before applying, you’ll understand what lenders see and can prepare confidently.

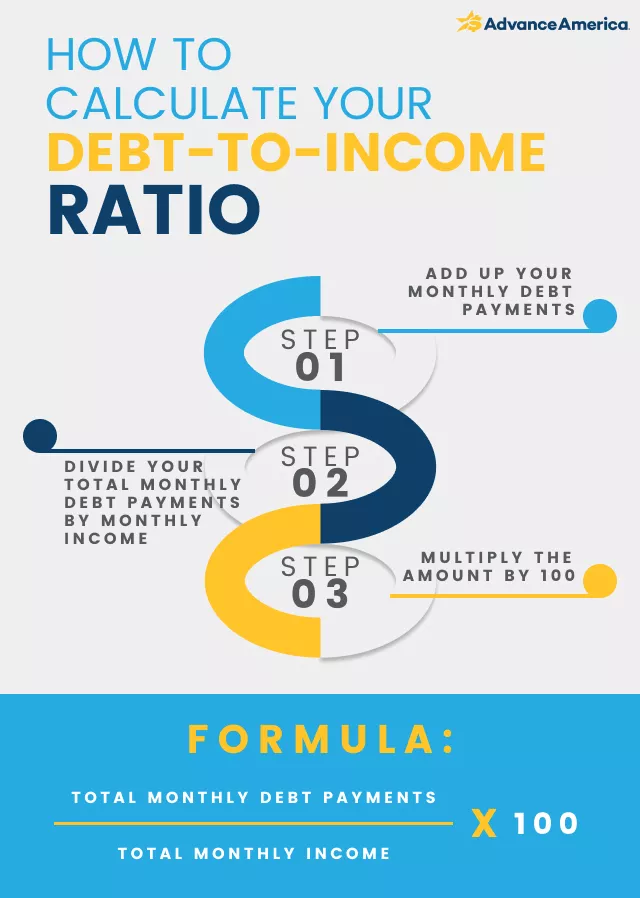

Calculating your DTI is simple and takes just three steps.

DTI formula = (Monthly Debt ÷ Gross Monthly Income) × 100

Let’s say that your total monthly debt payments add up to $1,500, and your gross monthly income is $5,000.

$1,500 ÷ $5,000 = 0.30 → 30% DTI

A 30% DTI means 30 cents of every dollar you earn goes toward debt.

To correctly calculate your debt-to-income ratio, you need to know exactly which types of monthly payments are included and which aren’t.

Included:

Not included:

Keeping track of these categories can help you see where your money’s going and where you might find opportunities to lower your ratio.

➢RELATED: Good Debt vs. Bad Debt

Most lenders look for a DTI below 36%. That typically signals a balanced, healthy financial profile. Ratios above 43% can limit your borrowing options, especially for large loans like mortgages.

Here’s a quick comparison chart of DTI ranges:

| DTI range | What it means | Borrower outlook |

|---|---|---|

| Under 36% | Good | Healthy debt balance, strong loan approval odds |

| 36-43% | Fair | Manageable, but may limit some options |

| 44-50% | High | Could affect loan approval or interest rates |

| 50%+ | Risky | Time to rebalance debt vs. income |

Different loan types come with different expectations:

There’s no single “perfect” DTI. What matters is understanding where you stand and taking steps to keep your finances healthy.

Your debt-to-income ratio affects more than loan approvals. It influences the interest rates, loan terms, and credit opportunities available to you.

A lower DTI generally means:

A higher DTI may mean you’ll pay more interest or face stricter borrowing limits.

If your DTI is higher than you’d like, don’t worry. Small changes can make a big difference.

Focus on credit cards or loans with the highest interest rates. Paying these off first — known as the avalanche method — reduces both your monthly payments and overall interest over time.

Alternatively, try the snowball method: Pay off your smallest debts first for quick wins and motivation.

➢RELATED: How to Get Out of Debt

Even a modest income boost can improve your DTI. Consider:

Each new dollar earned can slightly lower your DTI percentage, giving you more financial breathing room.

➢RELATED: Need Money Now? 13 Ways to Get Cash Today

If you’re planning to apply for a loan soon, avoid taking on new debt beforehand, as it can raise your debt-to-income ratio and hurt your chances of approval.

Consolidating multiple debts into a single payment can simplify budgeting and lower your monthly payments, improving your DTI. Make sure to compare rates and terms, and confirm that the new loan’s total cost works in your favor.

Many people start out with a higher debt-to-income ratio, and that’s okay. The important part is having a plan to lower it.

Here are a few practical steps:

💡 Tip: Progress often happens gradually. Celebrate each small reduction in your DTI as a win toward greater stability.

Yes, rent counts as a debt obligation because it represents a recurring monthly payment tied to housing.

DTI looks at your debt payments vs. income, while credit utilization is how much of your credit limit you're actually using. Both matter, but they measure different things.

It’s possible. Some lenders consider additional factors like credit score, income stability, and savings. However, you may face higher rates or need a co-signer.

Check your ratio whenever your income or debts change to stay aware of your borrowing power.

Remember: DTI is not a judgment — it’s just information. The goal isn’t to be perfect, but to be aware and make progress over time.

When you understand your DTI, you have a clear picture of your finances, which lets you borrow with confidence and build a strong financial future.

More financial empowerment:

Notice: Information provided in this article is for informational purposes only. Consult your attorney or financial advisor about your financial circumstances.

Bree Ewers is a senior editor, copywriter, and content writer whose work has been featured across the media, small business, and financial industries. She operates Nomad Freelance Content from her home office in Portland, Oregon.